Many of you have expressed concern about increasing taxes with the current administration. On September 13, 2021, we got our first real glimpse at what the future tax environment could look like in the coming years, as Biden’s Tax Proposal was released by the Democrats on the House Ways and Means Committee.

The legislation addresses a wide range of tax issues, all of which we will not cover here, however, we have included the following as most relevant to the clients we serve:

- Increasing the top ordinary income tax bracket,

- Cracking down on popular retirement account strategies, and

- Bringing the estate and gift tax exemptions back to pre-2017 levels.

The bill includes a host of new tax increases that will largely affect those households earning more than $400,000.

Top Income Tax Rate:

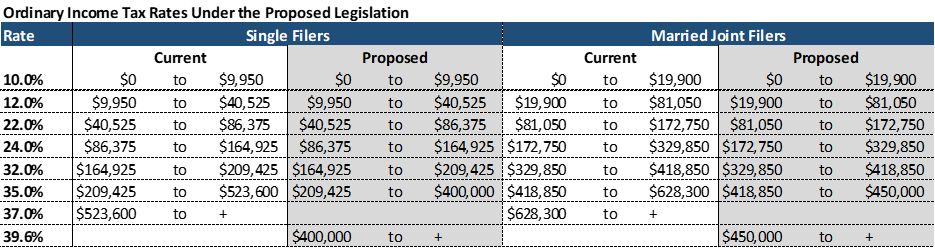

If enacted, the current bill would reinstall 39.6% as the top ordinary income tax rate, beginning in 2022. This rate was the top rate from 2013-2017, and then was reduced to 37% in 2018 with the Tax Cuts And Jobs Act of 2017.

Of important note is the fact that the Tax Proposal does not simply replace the current 37% bracket with the new 39.6% bracket, but rather, it also significantly lowers the amount of income a taxpayer can have before finding themselves in the top tax brackets. So, while it is true that most households earning below $400,000 will not be affected, more households that sat comfortably in the 35% tax bracket, will now find themselves pushed into the highest tax bracket because the ranges have been so compressed.

Please see the chart below that shows the current income tax ranges versus the proposed ranges under the bill. As you will see the income tax ranges will affect anyone in the current 35% tax bracket and up:

- It stands to reason that those with the highest income could benefit the most from accelerating that income now, before 2022.

Top Long-Term Capital Gains Rate:

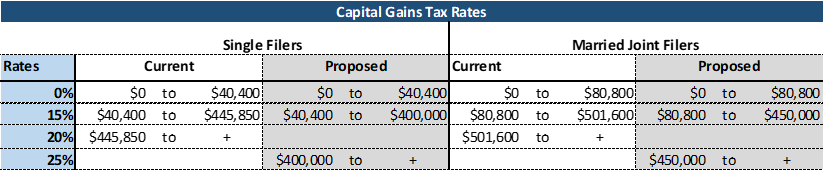

Also included in the proposal is a new long-term capital gains rate of 25%.

WARNING: The proposal for the long-term capital gains rate is to take effect retroactively back to September 13, not at the beginning of 2022. If passed in this form, taxpayers with large unrealized capital gains would not be able to sell such assets before the end of the year to avoid the higher rate.

Please see the chart below showing the new long-term capital gains rates:

Prohibition On Conversions of After-Tax Amounts:

If enacted as proposed the bill will prohibit conversions of after-tax dollars held in retirement accounts (both IRAs and employer-sponsored retirement plans, such as 401(k)s), beginning in 2022. What this part of the bill means is that Congress is trying to eliminate the “Backdoor Roth” strategy.

A Backdoor Roth is a way for people with high incomes to sidestep the Roth’s income limits. Those with higher income who are not able to make a Roth IRA contribution are able to effectively work around the income thresholds by making a non-deductible IRA contribution (permissible even at high income levels) and then converting it to a Roth. You do the following:

- Contribute to non-deductible IRA,

- Invest funds in the non-deductible IRA,

- Keep invested for 1 year, and

- Convert to Roth IRA.

Even though you did not qualify to contribute to a Roth because your income was too high, you get to go in the backdoor anyway.

- If you have been waiting for the optimal time to make a Roth conversion, the choice may soon be now or never (at least with respect to the after-tax dollars in an IRA account).

No Conversions for High-Income Earners:

For taxpayers with Adjusted Taxable Income in excess of applicable thresholds, the bill would prohibit Roth conversions altogether. Adjusted Taxable Income would be equal to Taxable Income, plus any deduction for contributions made to an IRA, less any required minimum distributions due to high income/total retirement account funds The thresholds for Adjusted Taxable Income are as follows:

- Single filers – $400,000

- Joint filers – $450,000

Get This:

Whereas most of the proposals in the bill are designed to curtail various practices by high-income taxpayers and would go into effect beginning in 2022, the prohibition on conversions for high-income taxpayers would not take effect until 2032.

We think you would agree, this provision is curious. Why would Congress delay the effective date so long for something they clearly want to ban?

As I often say to my kids, “Follow the money!” By allowing Roth conversions for high-income taxpayers for another decade, legislators can count on the income from those conversions for budget projections (which, not coincidentally, go out 10 years).

Reduction in the Estate and Gift Tax Exemption:

The Tax Cuts and Jobs Act changed the unified estate and gift tax exemption from (an inflation-adjusted) $5 million to $10 million, beginning in 2018. Although that change was scheduled to sunset automatically at the end of 2025, the proposed bill shifts forward that timeframe, reducing the exemption amount back to (an inflation-adjusted) $5 million for 2022 and future years, which is expected to be about $6 million in 2022 after inflation adjustments.

Conclusion:

There are a myriad of other provisions in the proposed bill, and nothing has been finalized at this point. However, it appears that Congress has already compromised internally on many of these matters since the proposal does not include some rumored measures, such as equalizing the top ordinary income and capital gains rates or eliminating the step-up in cost basis when an account owner passes away.

- Thus, we think the current “American Families Plan” tax proposal will likely not change substantially from where it stands now. Only time will tell.

We hope you found this breakdown helpful.

Written by: Jamie Runey, Founder and CEO at Runey & Associates Wealth Management