Introduction to NUA Tax Treatment

Are you looking for Retirement Planning Strategies for Boeing Employees? If you’re a Boeing employee nearing retirement, it’s essential to understand all your options for maximizing your retirement income. One strategy you might not be familiar with is the Net Unrealized Appreciation (NUA) tax treatment. Unlike simply rolling your 401(k) into an IRA, the NUA strategy allows you to transfer the appreciated value of your Boeing stock to a taxable brokerage account. This can result in significant tax savings over time. By leveraging the NUA tax treatment, you could pay long-term capital gains tax rates on the appreciation, which is often much lower than ordinary income tax rates. This approach can potentially increase the money available for your retirement activities.

Understanding the Benefits of NUA

Depending on your circumstances, the NUA tax treatment may allow you to pay a lower tax rate on the appreciation of your Boeing stock, offering significant financial advantages. Typically, distributions from 401(k)s and Traditional IRAs are taxed as ordinary income, which can reach up to 37% under current federal tax brackets. By leveraging the NUA strategy, the growth portion of your Boeing stock is taxed at the more favorable long-term capital gains rates, ranging from 0% to 20%. Many retirees find themselves in the 15% long-term capital gains tax bracket, which results in substantial tax savings. This approach frees up more of your retirement income, enabling you to enjoy your post-career years with greater financial flexibility.

Executing the NUA Strategy

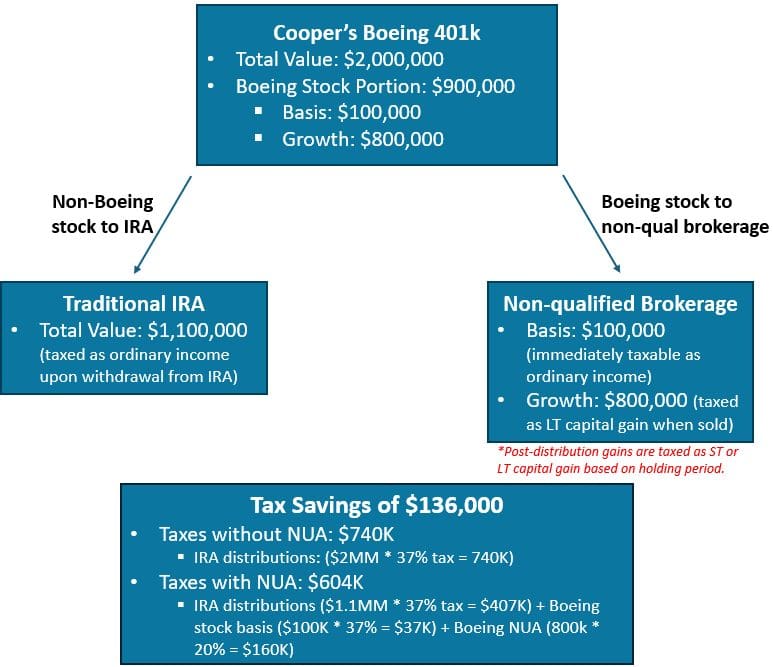

To utilize the NUA tax treatment, you must execute a lump-sum distribution of your 401(k). This involves transferring your Boeing stock to a non-qualified brokerage account, while rolling the remaining 401(k) funds into an IRA. During the year of this distribution, the original cost basis of the Boeing stock will be taxed as ordinary income. The growth portion, however, will be taxed at long-term capital gains rates when sold, offering potential tax savings. If you are under age 59.5, be aware that a 10% penalty for premature distribution may apply, which could affect the overall benefits of this strategy. Careful planning and professional advice are essential to maximize the advantages of this approach.

NUA Example: Retirement Planning for Boeing Employees

Weighing Risks and Benefits

While the NUA tax treatment can provide substantial tax savings, it’s essential to consider the associated risks. One primary concern is the concentration risk of holding a significant portion of your retirement savings in Boeing stock. Market volatility can impact the value of your shares, potentially jeopardizing your financial security if the stock performs poorly. Diversification is a fundamental principle of investing, and over-reliance on a single stock can undermine this strategy.

Another risk to consider is the timing of the distribution and sale of your stock. The value of your Boeing shares at the time of distribution will affect your overall tax liability. If the stock’s price drops significantly before you sell, the anticipated tax savings could be reduced. Additionally, the NUA strategy involves immediate taxation of the original cost basis of the stock as ordinary income. This could push you into a higher tax bracket for that year, increasing your tax burden.

It’s also crucial to consider your broader financial situation, including other sources of retirement income and your overall investment strategy. The benefits of the NUA treatment should be weighed against the need for a diversified portfolio that can withstand market fluctuations. Engaging with financial advisors can help you evaluate the potential tax benefits in the context of your overall retirement plan, ensuring that your investment decisions align with your long-term goals.

Given the complexities involved, it’s advisable to conduct a thorough analysis and consult professionals to understand the potential risks and benefits fully. This approach helps ensure that your retirement strategy remains balanced and resilient, even if market conditions change.

Working with Professionals

Navigating the intricacies of the NUA tax treatment can be daunting without professional assistance. Experienced financial advisors and tax professionals can provide invaluable guidance tailored to your unique circumstances. They will help you assess whether the NUA strategy aligns with your financial goals by analyzing your current tax situation and projecting future tax implications. Professionals can also assist in planning the timing of your lump-sum distribution to minimize tax liabilities and avoid penalties.

Additionally, they can help you balance the risks associated with holding a large concentration of Boeing stock by advising on diversification strategies. By working with experts, you gain the benefit of their knowledge and experience, ensuring that every step you take is optimized for your financial well-being. They can also help you understand the implications of the NUA strategy on your overall retirement plan, ensuring it complements other income sources and investment strategies. Engaging with professionals allows you to make informed decisions, leveraging their expertise to navigate the complexities of tax laws and investment planning effectively.

Conclusion: Retirement Planning for Boeing Employees

If you hold highly appreciated Boeing stock and are approaching retirement, the NUA tax treatment could be a valuable strategy to explore. This approach offers the potential for substantial tax savings by allowing you to pay long-term capital gains tax rates on the appreciation of your Boeing stock rather than the higher ordinary income tax rates. However, the complexities involved in executing this strategy make it essential to consult with experienced financial and tax professionals. They can help you assess whether the benefits of the NUA strategy align with your overall financial goals and retirement plans.

* This article is provided for informational purposes only and is not intended to be considered as tax, legal, or investment advice. The example included (Cooper) involves assumptions and may not account for all possible tax implications, such as net investment income taxes, the impact of the stocks potential increase or decrease in value, potential change in tax rates and tax laws, etc.