In the final days of 2022, the U.S. House of Representatives passed a spending bill known as the Consolidated Appropriations Act of 2023. A major part of this spending package includes a retirement bill referred to as the SECURE ACT 2.0, which may have major implications on your retirement.

While there are hundreds of provisions included in the SECURE ACT 2.0, there are three major changes impacting those in or nearing retirement:

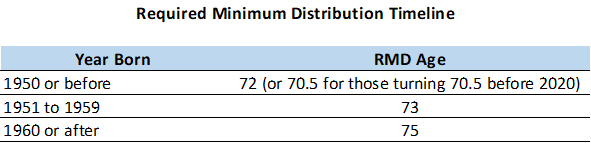

1. The Required Minimum Distribution (“RMD”) Age is Changing to 73…for Now

After allowing you to defer paying taxes into your retirement accounts and traditional IRA’s, Uncle Sam eventually comes knocking to collect his taxes.

This tax is achieved by establishing a minimum amount you must withdraw from your non-Roth retirement accounts each year (which you pay income tax on). In the three years leading up to the passing of SECURE ACT 2.0, the RMD age was 72.

Good news – those of you who were born between 1951 and 1959 can now delay taking RMD’s until the year you turn age 73. Further, individuals born in 1960 and later will now be allowed to delay taking their RMD’s until age 75.

If you were the unfortunate soul turning age 72 on December 31, 2022, you will still be required to continue RMD’s under the existing rules (beginning at age 72) and will have to take an RMD for 2022 and each year thereafter. Furthermore, if you turned age 70.5 prior to 2020 you will have had to begin taking RMD’s in 2020 and each year after.

If you were born in 1951 or after, and if your cash flow situation allows it, it may be wise to take advantage of these extra year(s) of tax-deferred growth in your retirement accounts. It is a great time to lower your lifetime tax bill with a series of partial Roth conversions.

2. SIMPLE IRA & SEP IRA Roth Options

Since the inception of the SIMPLE and SEP IRA’s, all contributions had to be made pre-tax, which meant the eventual withdrawals from these retirement accounts (i.e., at RMD age discussed earlier) were fully taxable as normal income. Provisions in the SECURE Act 2.0 have done away with this provision, allowing for Roth contributions to SIMPLE and SEP IRA’s to begin in 2023.

This is fantastic news for those with a SIMPLE or SEP IRA who are in a low marginal tax bracket and want to recognize some income now, or those looking to diversify their retirement withholdings between a Roth and Traditional allocation.

While most would agree the creation of a Roth option for SIMPLE an SEP IRA’s is a good thing, you may be disappointed if you call your custodian today looking to establish and contribute to one of these Roth accounts. It will likely take several months before further guidance has been provided by the IRS and employers have set up plan documents for these types of retirement accounts – so stay tuned.

3. Catch-Up Provisions Changes

The Secure Act 2.0 has several measures incentivizing saving more in retirement accounts, including changes to catch-up contributions, which are additional contributions permitted for people age 50+. Three of the changes that will likely have a wide-spread impact on those nearing retirement include:

- Catch-up contribution limits on IRA’s will be indexed to inflation beginning in 2024. Currently, the amount is a fixed $1,000 per year.

- Catch-up contribution limits on 401(k)’s and 403(b)’s will be increasing to the greater of 150% of the standard catch-up contribution amount for 2024 or $10,000 for those age 60 to 63. Currently, the catch-up amount is $7,500. Like the IRA, the amount will be adjusted for inflation beginning in 2024.

- SIMPLE Plan participants age 60 to 63 will see a catch-up contribution increase to the greater of 150% of the standard catch-up contribution amount for 2025 or $5,000. Additionally, the deferral and catch-up amount is being increased by 10% in 2024 for those employers with 50 or fewer employees.

Important note: one change being implemented that high earners should be aware of is the “Rothification” of catch-up contributions. Beginning in 2024 high wage earners (defined as those earning $145,000+ from one employer in the previous calendar year) will be required to make any catch-up contributions on an after-tax basis. Unfortunately, this means having to pay more tax up front on the catch-up contributions. On the plus side, these individuals will get to take advantage of tax-free growth because of the Roth catch-up contribution.

For the time being, it appears this rule does not apply to self-employed individuals.

In Conclusion

There are hundreds of provisions passed through the SECURE Act 2.0 that may impact your financial life. While this blog highlights a few of the most significant changes for those in or nearing retirement, it may be wise to reach out to a financial advisor to see what investment or tax planning opportunities are available to you in relation to the passing of the SECURE Act 2.0.